This is an electronically generated document which should be generated when goods worth more than Rs.50,000 is moved from one place to another, irrespective of whether the movement is inter-state or intra-state. This has to be carried by the person in charge of the conveyance carrying the consignment of goods. This document generated online has been made compulsory from 1st Feb 2018.

This electronically generated document (E-Way bill) under the GST Regime replaces the physical document required earlier for the movement of goods under the VAT regime. The person should log in using their GST account and provide the details of the consignment on the GST Common Portal in two sections (parts) of the bill.

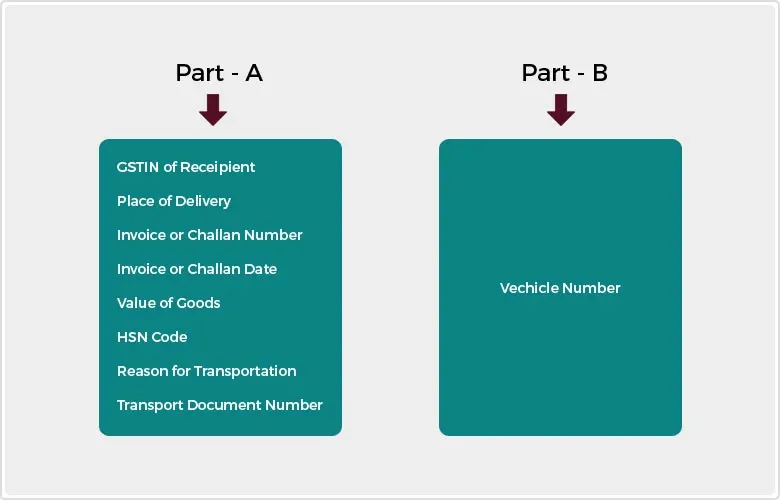

Part A of the E-Way Bill in Form EWB-01 collects the details of consignment i.e. the invoice details along with the reason for transportation which has to be selected from a list of available options.

In the Part B of the E-Way Bill the vehicle number in which goods are transported needs to be mentioned. This has to be provided by the transporter in the common portal. It is possible for one e-way bill to go through multiple modes of transportation before reaching the destination. Every time the mode of transportation changes the details of the new vehicle has to updated in it by using "Update Vehicle Number". Based on the information provided, an E-Way bill of this format would be generated.

The e-way bill under the GST Regime is required to be generated in all scenarios involving movement of Goods worth exceeding Rs.50,000. The transaction can be Sales, Sales Return / Branch transfer or inward supply. There can be two different situations here depending on the parties involved in the transaction

In case of movement by registered person

Registered person, be it the seller or the recipient of supply may generate the e-way bill in Form GST EWB 01 electronically on the common portal after furnishing information in Part B of Form GST EWB01, irrespective of whether the delivery happens in own conveyance or a hired one by road / railways / air or by vessel.

In case the movement of goods is caused by the registered person and handed over to the transporter for transportation by road, but has not generated the e-way bill, then the responsibility to generate it would belong to the transporter. The registered person should provide the details about the transporter in Part B of Form GST EWB 01 on gst.gov.in and then the e-way bill shall be generated by the transporter on the basis of the information provided by the registered person in Part A of Form GST EQB 01.

In Case of sale by unregistered person to Registered Person

In case of receipt of goods from an unregistered person, either the recipient of supply or the transporter should generate the e-way bill.

Validity period of e-way bill

The e-way bill thus generated will be valid only for a specific period:

| Distance | Validity Period |

|---|---|

| Less than 100 KM | 1 Day |

| For every 100 KM or part thereafter | 1 Additional Day |

When multiple consignments are transported in one conveyance, the transporter has to generate a consolidated e-way bill in Form GST EWB 02 on the GST website prior to moving the goods. He has to indicate the serial number of each individually generated e-way bill for each consignment and should generate the consolidated e-way bill

| No. of E-Way Bills | |

|---|---|

| E-Way Bill Number | |

Let us throw some light on the impact of e-way bill on the logistics industry. According to Mr.Hasmukh Adhia, Finance Secretary, the e-way bill filing promises better revenue using the benefits of Information Technology. It is also expected that the E-way bill mechanism would be an effective tool to track movement of goods and check tax evasion and will ensure that goods being transported comply with the GST Law.

The E-Way Bill promises multiple benefits for the transporters. The advantages of E-Way Billing can be summarized this way:

No more Cumbersome Documentation - All the existing state-wise documentation required for movement of goods will no longer be required. Another beneficial option that is available for the transporters is the installation of RFID device in the vehicle used to transport consignments on a regular basis. The person in charge of the vehicle no longer has to carry physical copies as the device is attached to the vehicle and the e-way bill can be mapped and verified through the device itself.

Quicker movement of Consignment - Another big advantage of E-Way Billing will be the removal of the large number of check-posts across state borders and national highways, resulting in ease of movement of goods.

Reduced Logistics Cost - E-Way Bill would reinforce proper invoicing and this way would reduce tax evasions. In the longer run this bill is expected to reduce our Logistic cost to GDP ratio, which is currently very high when compared to other nations.

However there are some bottlenecks which are issues of concern for the logistics industry. Putting the disadvantages of E-Way Billing in a nutshell we have :

Accessibility / familiarity to IT Infrastructure – Small transporters especially from rural areas will face difficulty in securing access to GSTN portal for generating the e-way bill. The government now faces the mammoth task of ensuring that all transporters big or small from rural or urban areas do have access to internet even on the go.

According to KPMG, Indirect Tax Partner, Priyajit Ghosh, "Unless a company has the IT system to support and generate way bills in real time, it will be a huge issue. We have very less time to get the necessary infrastructure up". (Ref. Article)

Strict timelines for validity of e-way bills. The guidelines lied for E-Way validity have been remarked to be unrealistic by some industry experts. For example an e-way bill generated for a distance of 1000 kms is valid only for ten days from the date on which it is generated. However research indicates that the average speed of Indian truck drivers is 20-40 km/hour, and the average distance covered daily is 250-400 kms. Moreover when heavy machinery like a Boiler or big equipment like wind mill blades are transported on a specialized truck, the number of days it may take for it to cover 500 km can be much more than 10 days.

Maintaining multiple bills – E-com retailers use several modes of transport to ensure that goods reach the customers from the warehouse or the manufacturer’s location on time. Since a fresh e-way bill must be generated every time the mode of transport is changed E-com will definitely end up generating a large number of bills for every shipment.

Potential delays in generating e-way bills - Many a times customers end up cancelling orders even while the goods are in transit, or return goods already purchased. Fresh e-way bills have to be generated each time this happens. This poses an issue for E-com retailers who use third party logistics. They will be able to generate e-way bills only after the transporter also uploads details on the GSTN, which can cause potential delays in shipment.

There is mixed reaction from the industry regarding the implementation of the E-way bill. Some contemplate that this can create complications for transporters as it adds a layer of complexity to the whole process of shipping goods from one state to another. It also adds to the burden of the GST Network (GSTN)

Mr. Pratik Jain, Leader, Indirect Tax, PwC India feels that effective implementation of this system is important else it would lead to significant supply chain bottlenecks and could dilute the objective of "One Nation One Tax". (Ref. Article)

The AITAF (All India Tax Advocates’ Forum) seems to have a divided opinion in this issue, while some feel that this could make logistics more 'cumbersome and costly' while others are of the opinion that If implemented wisely, e-way bills have the potential to reshape the logistics industry and make transport of goods easier and faster.

Summing up, we find that there are expected positive impact of e-way bill and also visible loopholes in the realization of the vision of the bill. At this juncture when the e-bill is in the genesis stage, it will be too early to draw a conclusion as to whether the advantages of e-way bill outweigh disadvantages or vice-versa. Implementation is the key and that would decide what e-way bill would turn out to be!!